Analysis of free and paid channels for Airbnb, Booking, Despegar, Ctrip, eDreams, Expedia, Kiwi.com, Lastminute.com and MisterFly

Customer acquisition is a key driver for Online Travel Agencies (OTAs). In this post, I will look at how 9 OTA domains compare in terms of incoming traffic channels using SEMrush Traffic Analytics data. OTAs excel at capturing and consolidating demand at scale. They are best-in-class in traffic and customer acquisition not only in the travel sector but in the larger eCommerce category. It is important to understand where traffic is coming from, as this has a direct impact on the OTA’s ability to continue fueling traffic to the top of the funnel in a way that is profitable and building customer loyalty.

At a basic level, we can divide traffic in two main categories: Free and Paid. Some general considerations:

- A high share of free traffic can be a signal of

– Brand strength

– OTA with a unique product/service

– Path to becoming a travel aggregator

– Lack of paid marketing push if it’s accompanied by flat of decreasing growth - The higher the share of free traffic, the better the OTA is positioned to aggressively invest in acquiring traffic (and growth).

- A high share of profitable paid traffic can be a strong competitive advantage, particularly if it’s coupled with high growth.

- A high reliance on the metasearch channel is dangerous for OTAs as it commoditizes the underlying product and it adds quality content to a competitor. In a metasearch-originated booking, customer loyalty generally flows to the metasearch. And if there is a problem with the booking or trip, it is the OTA that takes the hit.

Free / Low cost / Branded Subcategories

– Direct: visitors typing the URL directly in the browser or reach via browser bookmarks.

– Search Engine Optimization (also known as SEO or Organic): the unpaid links that show up in search result pages.

– Email: traffic generated from various CRM and newsletter activity

– Social: unpaid social media content posted by brand or general public.

– Branded Paid Search (Branded SEM): traffic coming search engines (Google) generated by keywords that contain your own brand. For example, Airbnb would consider branded SEM traffic coming from keywords such as “Airbnb” or “Airbnb Barcelona”. There is very little bidding competition for these keywords because the conversion for any competitor that is not Airbnb would be very low, since the person searching has already signalled that they want to transact with Airbnb.

Paid Subcategories

– Non-branded Paid Search (non-branded SEM): traffic coming from search engines generated by keywords that do not contain the business’ brand. For example, “hotels in Paris”, “flights Barcelona New York”.

– Metasearch: presence in metasearch engines such as Jetcost, Kayak, Skyscanner, Momondo, etc…

– Affiliate marketing

– Strategic partnerships: providing technology solutions and product to travel industry players such as travel agencies, airlines, hotels, OTAs and corporates.

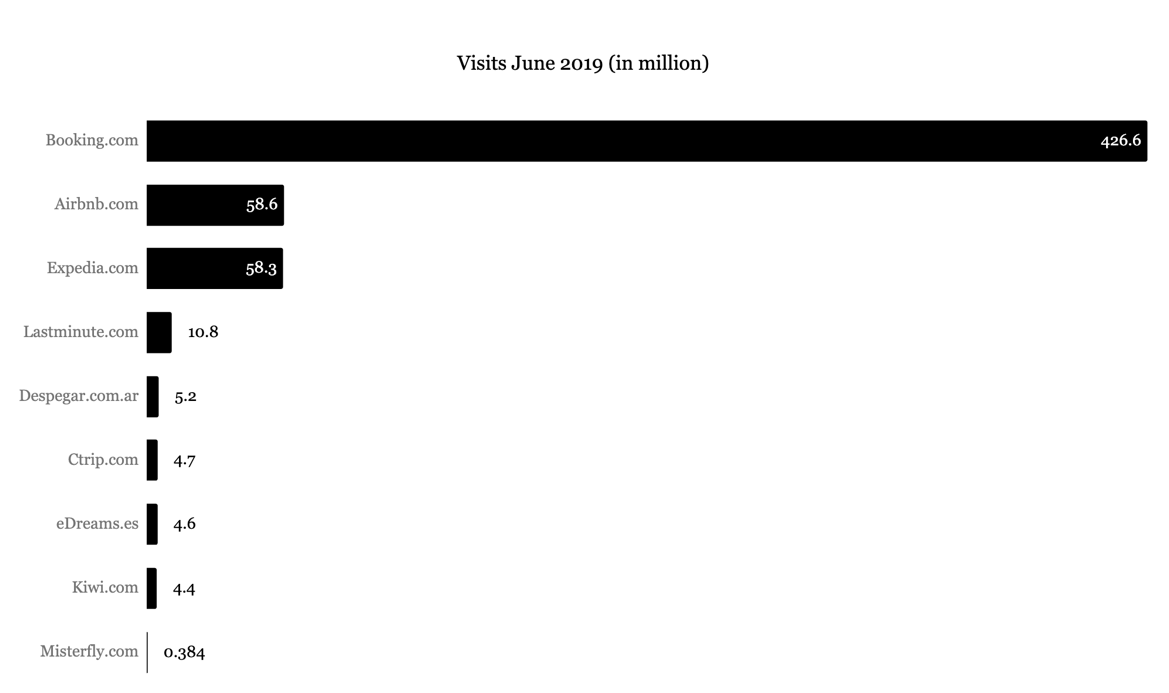

Visits

I am looking at data from only one domain for each of the OTAs. Some of these websites have country code top level domains (i.e. eDreams.es applies to eDreams’ Spain business, Despegar.com.ar applies to Despegar’s Argentina business, etc…) and others consolidate all their countries activity in one unique global domain (such as Booking.com, Airbnb.com, Kiwi.com, Lastminute.com).

There is a great difference in monthly traffic among these 9 domains, as we can witness in this graph:

I looked at the data and aggregated the various traffic sources and mediums into the channel subcategories previously defined (Note 1).

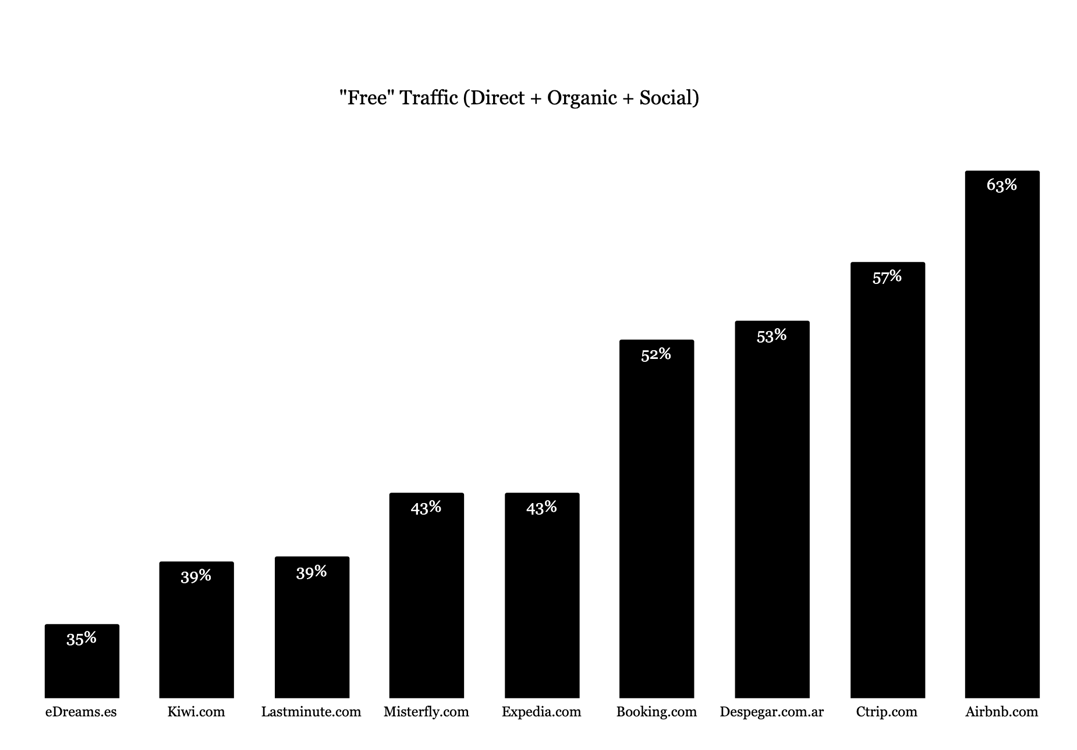

Free/Low Cost Traffic

Let’s first see how the 9 OTA domains compare in terms of free traffic. This traffic is mostly driven by the power of the OTA brand and reflects a strong brand that is delivering value to the customer beyond being well positioned in search engines and metasearches. Of course, building a brand is not purely “free” at its origin, as it often has entailed costly offline and online campaigns.

All 5 European-based OTAs are on the lower side of free traffic. eDreams.es has the lowest share, with 35%. eDreams’ newly launched subscription service could be a step in the right direction. Time will tell if eDreams is able to improve its branded traffic share as a result.

Airbnb.com is on the other extreme, with 63% share of free or low cost traffic. Airbnb has clearly disrupted the accommodations industry by building a platform with a very differentiated product which has attracted a large number of direct visitors.

Also with very high free traffic is Booking.com as well as regional champions Ctrip.com (Asia) and Despegar.com.ar (Latin America).

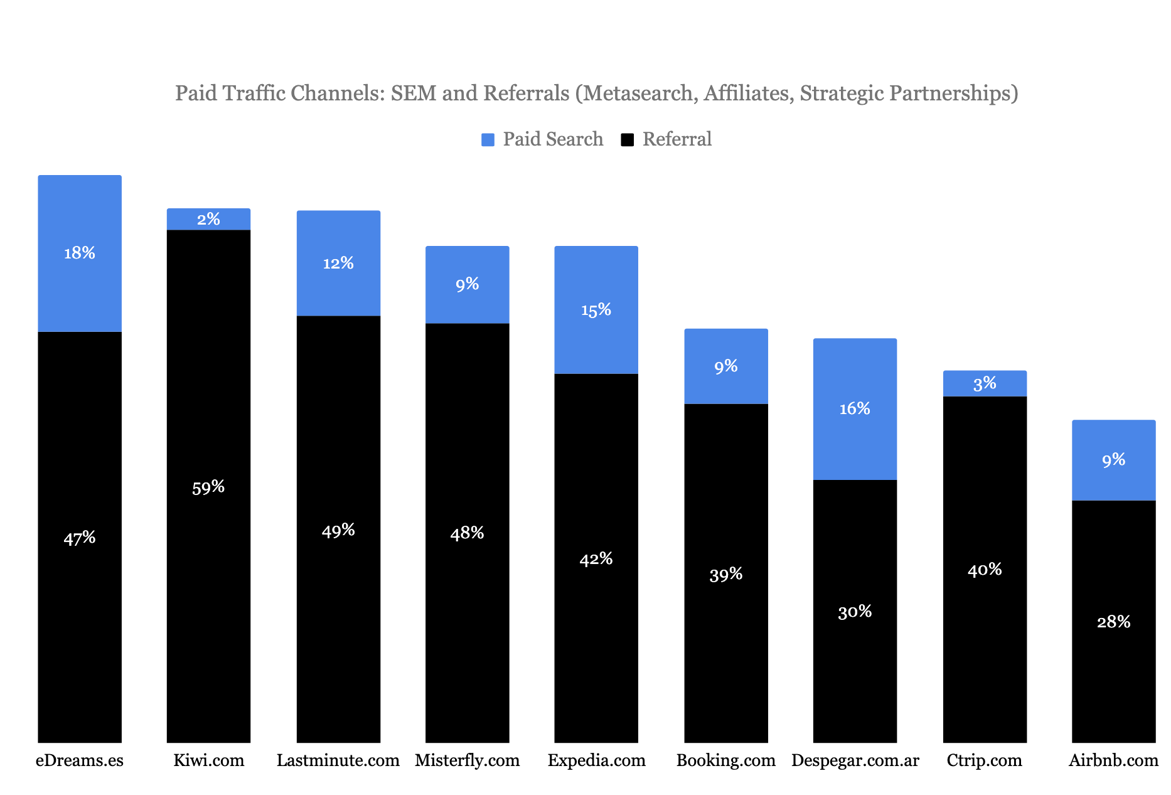

Paid Traffic

Paid traffic can translate into competitive advantages and recurrent business. This can be the case of strategic partnerships, for example:

– Booking.com powering Southwest Airlines’ hotel offering

– Misterfly.com providing flight services to Vente Privee members

– Kiwi.com’s partnership with the Cote d’Azur’s airport

– Lastminute.com powering Booking.com’s flight offering

eDreams has the highest share of paid traffic. Until 2014, eDreams underwent uninterrupted and double digit annual growth with an aggressive paid marketing strategy and based on sustained innovation in the flights sector. Being a market leader in flights requires constant innovation and intense focus in bringing a differentiated and unique product value. Since 2014 to 2019 however, eDreams’ EBITDA has had a CAGR of 0.3% and its ratio of marketing costs to revenue margin has worsened from 59% to 63%. A high share of paid traffic and low or flat growth is not a good combination.

Kiwi.com has also a high share of paid traffic, made up mostly of referrals and basically no SEM. Kiwi.com’s strong referral traffic is not only made up from metasearches, but from an increasing focus on strategic partnerships. Kiwi is expected to grow by 40% in 2019 by multimodal innovation (how to get travellers from point A to point B combining all relevant modes of transportation) and its focus on B2B strategic partnerships with already thousands of partners (airports, travel agents, airlines, consolidators) using Kiwi’s Tequila B2B platform.

Misterfly.com has almost half of its traffic coming from referrals. Misterly is undergoing strong growth through strategic partnerships, with an estimated 40% of their referral traffic coming from strategic partnerships with the likes of Vente Privee, Galeries Lafayette, BazarChic, Secret Escapes, Paris Airport, travel agency networks and others.

Despegar.com.ar and eDreams.es have one third of their traffic coming from Paid Search. Having scalable and efficient Google search campaigns is an important asset for OTAs, but they need to be able to capitalize on these customers so that they come back next time through branded non-paid channels. The problem lies when SEM is used as a transaction acquisition strategy with no impact on building customer loyalty.

Expedia and Booking manage among the world’s largest online marketing campaigns, with budgets almost reaching $5 billion each. However, they don’t have a relatively high share of paid traffic, compared to other OTAs. This is because they have managed to build a very strong product inventory and are benefiting from becoming dominant travel aggregators. Airbnb and Ctrip can certainly be included in the aggregator category as well.

A core precept of Aggregation Theory is that eventual-Aggregators start with some sort of insight into consumer preferences that allows them to deliver a superior user experience; this superior user experience acquires sufficient users that attract suppliers on the Aggregators terms, and the virtuous cycle begins — Ben Thompson, Stratechery

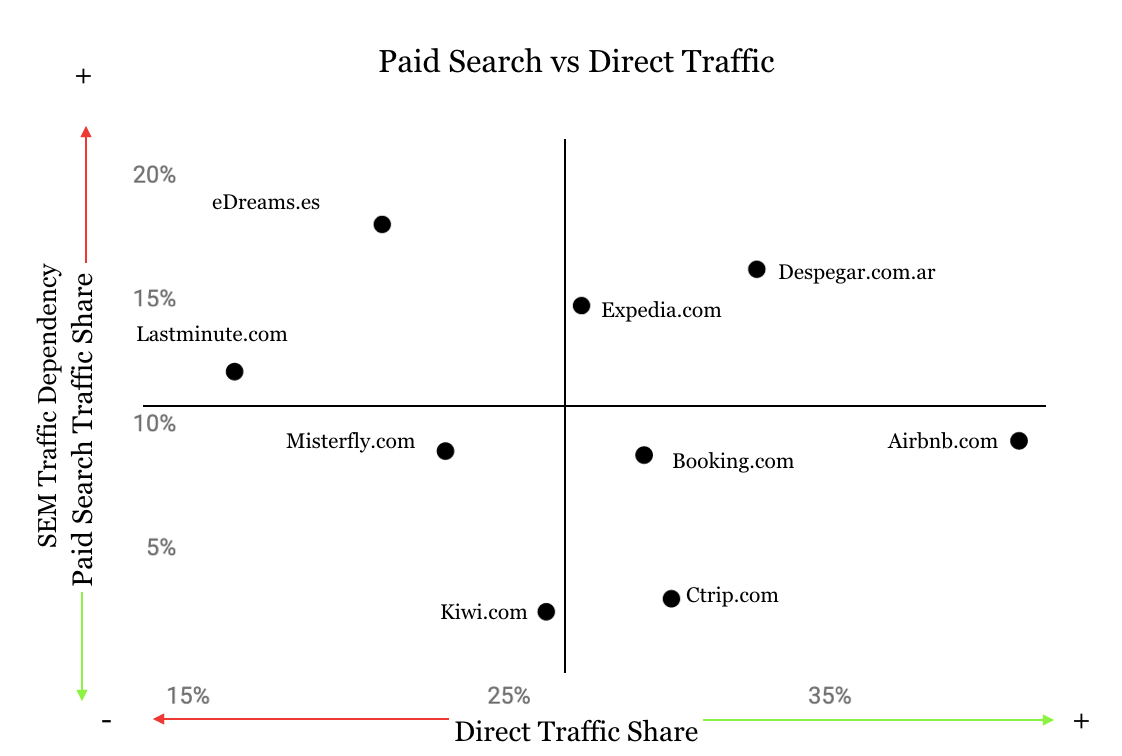

Spotting the Travel Aggregators

This is a very rough and dirty attempt to visualize OTAs’ relative brand power and traffic acquisition dependency. A better analysis would have to include profitability levels, annual growth rates and also would need to add branded organic and branded paid search to the free channel. But given that we do not have all this information, we’ll go with this insufficiente model.

The bottom right quadrant includes players with relatively lower paid search traffic dependency and higher direct traffic share. This is where aggregators would most likely be. Airbnb, Booking and Ctrip are in this quadrant. The absence of Expedia in this quadrant (it’s not too far, though) points to the inadequacies of this limited model.

I am a strong believer in the power of OTAs. With ever more product categories and pricing complexities, the value of retailers should be even greater as they can bring order to chaos. In this post, I have not focused much on the OTA’s product, which is essential to get customers to come back (hopefully directly). Maybe a topic for a a future post.

_________________________________________________________________

Sign up to Travel Tech Essentialist, a newsletter sent every two weeks with my pick of the top 10 news on the online travel ecosystem.

_________________________________________________________________

Note 1: I was not able to get detail in terms of branded or non branded keywords. Therefore, organic traffic includes both branded and non branded keywords. So does paid search traffic.