Full year 2018 results and key takeaways for 10 publicly traded online travel companies: Booking, Expedia, Ctrip, eDreams Odigeo, Despegar, On The Beach, Lastminute, MakeMyTrip, TripAdvisor, Trivago

All publicly traded online travel companies have reported their 2018 results. The first section of this report will cover how these 8 Online Travel Agencies and 2 metasearch companies compare in terms of revenue, EBITDA, Enterprise Value and marketing efficiency. In the second section, we will take a closer look at each company and highlight some of their successes and challenges.

Some highlights on the group’s 2018 results:

– Combined revenues grew at a weighed average of 11% and simple average of 6%.

– Booking and Expedia account for 79% of the combined revenue of the 8 OTAs in this report, as they continue to build up their non-traditional inventory to compete against the likes of Airbnb.

– All companies in the report have shown significant positive EBITDA figures for all the years in the reports and double digit EBITDA/Revenue margins ranging from 10% to 40% with the exception of:

- MakeMyTrip: With large and increasingly negative losses MakeMyTrip has never shown a profit and shows a worrying EBITDA/Revenue margin of negative 20%. This together with 20% negative revenue growth place MakeMyTrip as the worst performer in the group and in a different category by itself.

- Trivago: Trivago’s EBITDA/Revenue margin of close to 1% is an order of magnitude below its peers. Again, with a fall in revenue of 11% last year, this puts Trivago in the far from stellar category.

- Although Ctrip has shown stellar revenue and EBITDA growth over the period, its EBITDA/Revenue margin of 10% is the worst after MakeMyTrip and Trivago, and it is also the only company in the group (apart from MakeMyTrip) which has posted a year of negative EBITDA in the period studied.

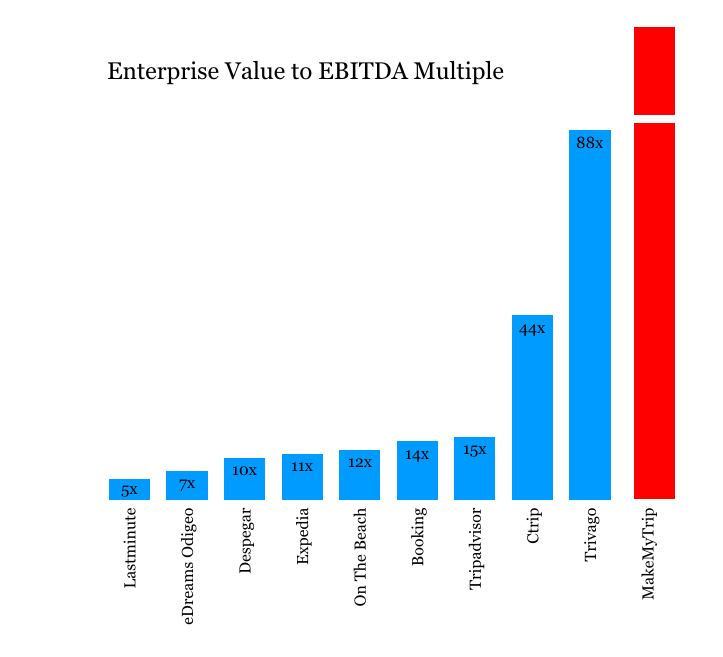

– MakeMyTrip’s and Trivago’s EV/EBITDA multiple shows an unusually high valuation, particularly when taking into account their challenges and underperformance.

– Ctrip and OnTheBeach saw the highest growth in 2018, and Lastminute also had a strong year with successes on its strategic goals as well.

– eDreams Odigeo remains the largest OTA in Europe in Revenue and EBITDA, but it is losing market share, growing at half the rate of the European online travel market. The other European OTA in the group, Lastminute Group, had a solid year of growth, with trends aligned with its stated strategic goals.

– The largest OTA in Latin America, Despegar, had a subpar year. Its results were particularly impacted by regional macroeconomic difficulties and currency fluctuations.

– TripAdvisor is 37% larger in revenues than Trivago, but 20X larger in EBITDA. Both are impacted by reduced investment by large OTAs like Expedia and Booking, but TripAdvisor’s EBITDA levels don’t compare with Trivago’s barely positive EBITDA (never above €28 million over the past 5 years.

1. 2018 Results

1.1. Revenues

Booking and Expedia account for 73% of combined revenues of the 10 online travel companies in this report, followed by Ctrip. The remaining 7 companies are responsible for 14% of total revenues.

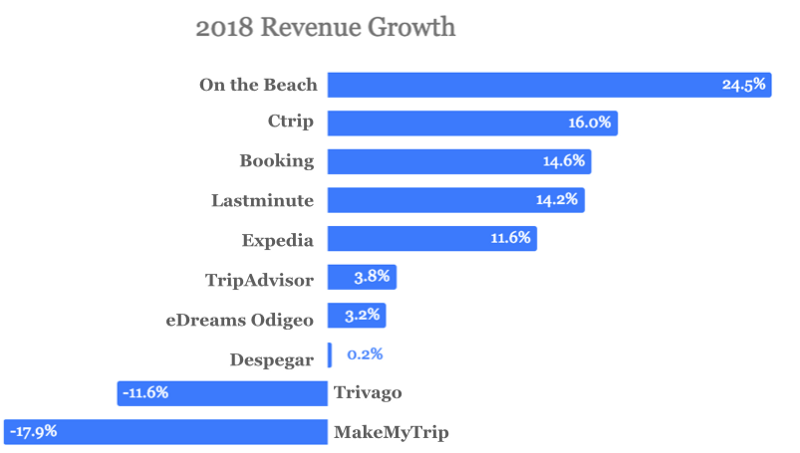

In 2018, five of the ten companies in this analysis had revenue growth above 10%, three grew below 5%, and two had revenue decreases of more than 10%. OnTheBeach had the largest revenue growth in 2018 (+24.5%), while the world’s largest OTAs — Booking, Expedia, Ctrip — had healthy double digit growth.

2018 was a bad year for metasearches, with TripAdvisor growing at 3.8% and Trivago falling by 17.9%. It was also a bad year for OTA regional champions, with MakeMyTrip (India’s largest OTA) at -17.9%, Despegar (Latin America’s largest OTA) barely growing at 0.2% and eDreams Odigeo (Europe’s largest OTA) growing by 3.2%. The one notable exception was Lastminute Group, which had a strong revenue growth of 14.2% .

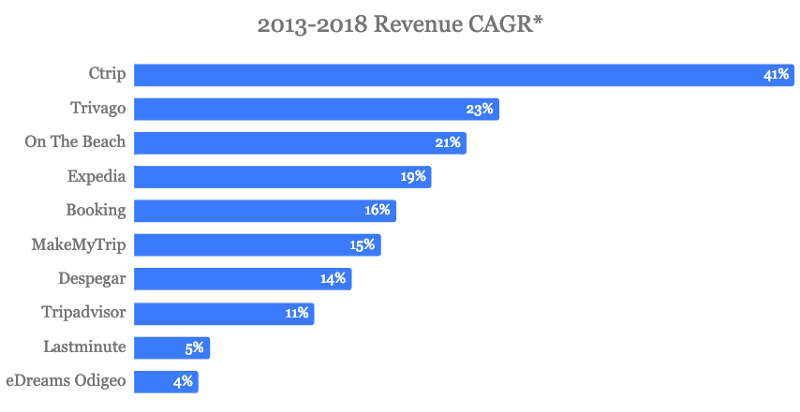

Taking a more long term view of revenue growth, we see that with the exception of Lastminute and eDreams Odigeo, all OTAs and metasearches in this analysis have had strong compounded annual growth rates well above 10%. Ctrip’s CAGR growth has been spectacular at 41%.

If we ignore the two metasearches and just look at the 8 OTAs in this analysis, the three largest (Booking, Expedia and Ctrip) concentrated 93% of total revenue for the 8 Online Travel Agencies.

1.2. EBITDA and Enterprise Value

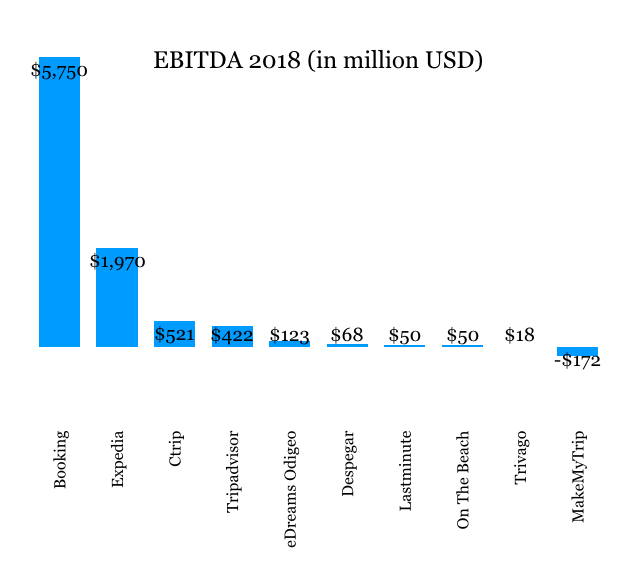

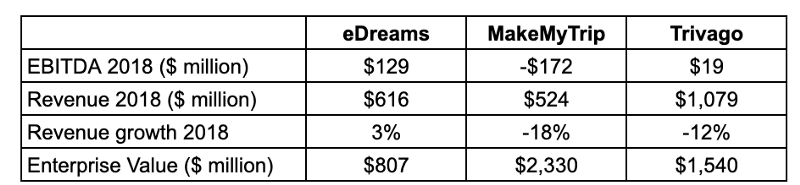

MakeMyTrip continues to be the only public online travel company posting EBITDA losses year after year. With a $172 million negative EBITDA, 2018 was no exception.

There is a very significant difference between the EBITDA of each of the world’s top 4 Online Travel Agencies. Booking leads by a very large margin with a 2018 EBITDA of $5750 million, followed by Expedia with $1970 million, Ctrip with $521 million and eDreams with €109 million.

Three Online Travel Agencies had EBITDA decrease from 2017 to 2018: Ctrip (-7%), eDreams Odigeo (-9%) and Despegar (-24%). Trivago had the largest percentage increase (+134%), followed by Lastminute (+60%). All others had strong EBITDA growth rates between 15% and 27%.

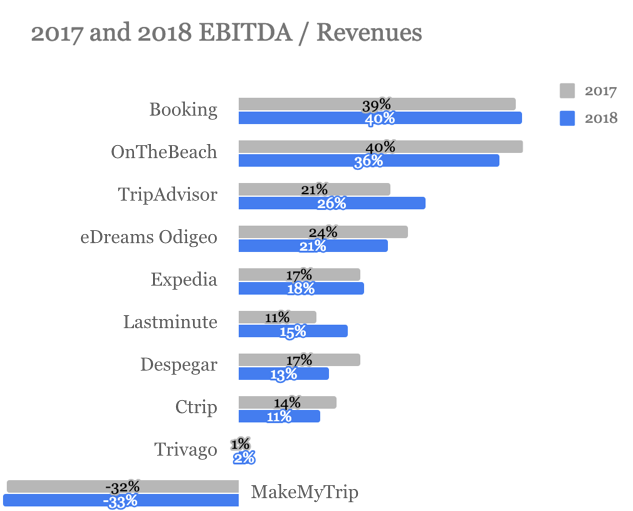

EBITDA margin (EBITDA/Revenues) is an assessment of operating profitability. At 40%, Booking comes up with the healthiest ratio. Vacation package specialist OnTheBeach also has a high EBITDA margin of 36%, 4 percentage points below 2017. With 21%, flight specialist OTA eDreams Odigeo has the third highest EBIDTA margin, although down from 24% in 2017. On the low end, Trivago is at only 2%, and MakeMyTrip is on negative territory.

It’s interesting to see how these companies compare from a perspective of the Enterprise Value to EBITDA multiple. EV is a measure of the company’s total value (market cap + debt – cash) and EV/EBITDA is a relevant trading multiple to evaluate companies that are trading cheap or expensive in relation to comparables. It very surprising to see the very high multiples of Trivago (88x) and MakeMyTrip (negative EBITDA, so ratio is not even applicable), particularly given the latter’s severe underperformance and negative EBITDA year after year. On the other end, Lastminute and eDreams Odigeo seem to be trading at a too low multiple for companies that, despite slower recent growth, have consistently been profitable with solid EBITDA and EBITDA margin.

It is difficult to understand how MakeMyTrip and Trivago can justify having a higher Enterprise Value than eDreams, when all the financials seem to point to the opposite direction. MakeMyTrip has been around for 20 years, and the prospects of potential future earnings are looking bleaker for a company that was founded 20 years ago and has not had a single quarter of positive EBITDA since 2012. Trivago’s business model seems fragile. Revenues are highly dependent on extremely high marketing spend, and Trivago’s EBITDA is slightly positive. eDreams on the other hand, has had continued revenue growth (albeit low) and has not had EBITDA below $100 million in the period analyzed in this report.

1.3. Marketing

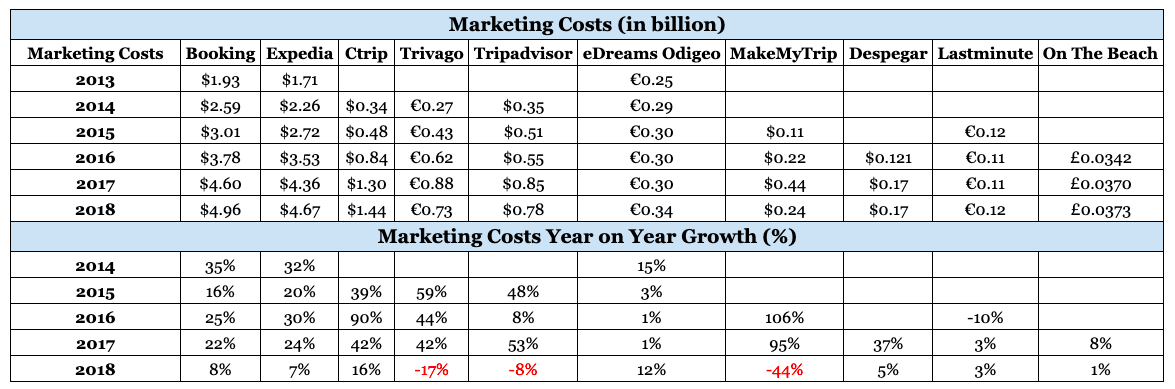

The two metasearch companies — TripAdvisor and Trivago — both lowered their marketing spend in 2018. The one OTA that also decreased its spend was MakeMyTrip. It decreased by 44%, equivalent to $200 million, which could explain its lower revenue in 2018, although its EBITDA margin worsened.

Ctrip had a 16% increase in marketing spend, mirroring its revenue growth. After three years of marginal increases, eDreams Odigeo’s marketing investment increased by 12% in 2018, but its revenues only grew by 3%.

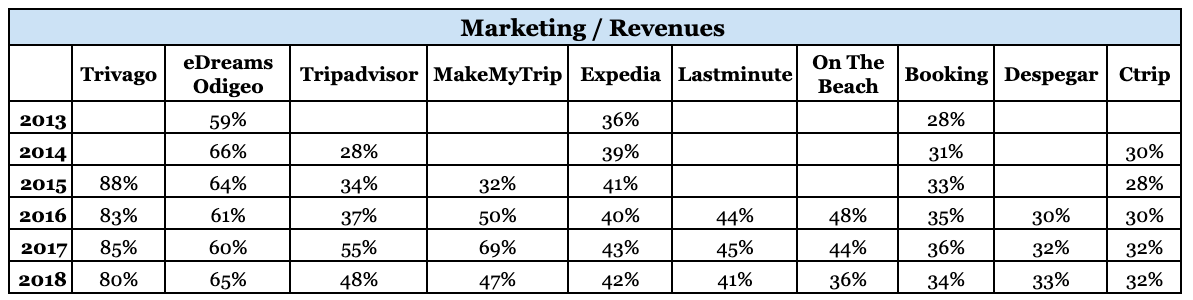

The marketing over revenues ratio can point to the relative efficiency of marketing spend. The higher the ratio, the more marketing pressure the company requires to drive sales, although we also need to take into account the nature of the product. Trivago, which has traditionally relied on extensive offline marketing campaigns had a very high 80% ratio in 2018, a slight improvement from previous years. eDreams Odigeo has the highest ratio of all OTAs, with 65%, which can be explained in some part to its flight product specialization. Expedia has been in the low 40’s for the past few years, while Booking has shown better marketing efficiency results in the low to mid 30’s. Ctrip (32%) and Despegar (33%) have the lowest ratios.

2. Key Takeaways

2.1. Booking Holdings

The world’s most valuable online travel agency delivers yet another high revenue growth year. Brands include Booking.com (primarily international), KAYAK, priceline (primarily North America), agoda (primarily Asia-Pacific region), Rentalcars.com and OpenTable.

The strength of Booking.com and its relentless focus on the accommodations product continues to fuel the group’s growth.

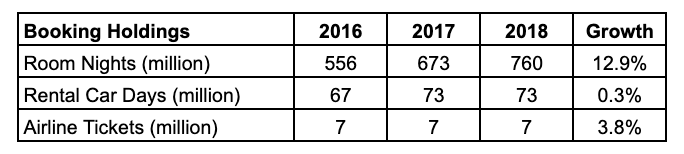

Booking continues to strengthen its position in alternative accommodations in order to compete effectively against Airbnb in this growing category. As of December 2018, 80% of Booking.com properties are homes, apartments and other non-traditional places to stay (in 2017 it was 75%). 2018 growth in non traditional properties was 47%, noticeably higher than the 10% growth in hotels, motels and resorts.

Booking Holdings’ business is driven primarily and increasingly by its international (outside the US) results, which consist of Booking.com, agoda.com and Rentalcars.com, and the international businesses of KAYAK and OpenTable. This classification is independent on where the consumer resides.

Share of International (non-US) Revenues*

2015: 80%

2016: 84%

2017: 87%

2018: 89%

* International revenues consist of Booking.com, Agoda and Rentalcars.com and the international businesses of KAYAK and OpenTable. This classification is independent of where the consumer is located.

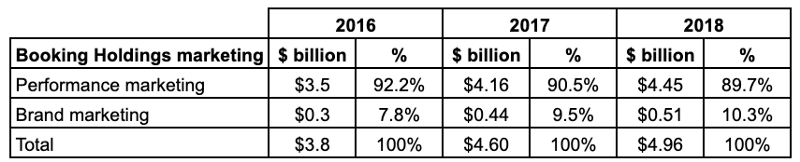

Booking Holdings’ marketing continues to be heavily focused on performance marketing (search, metasearch…), with 89.7% of its total marketing spend. The company announced at the end of 2017 an intention to shift more towards brand advertising (TV, online video, online display), but its brand marketing share in 2018 is only slightly above 10%, less than 1 percentage point above what it was in 2017.

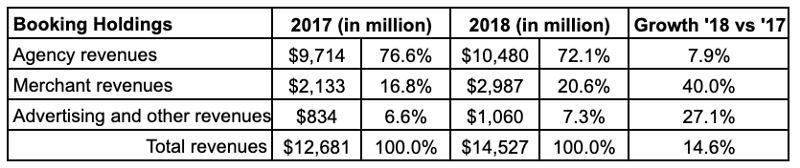

Booking.com has been expanding its merchant model (where Booking receives payments from travelers) to provide greater payment options for both customers and travel providers. Merchant revenues grew 40% in 2018, significantly above the 7.9% of agency revenues. It is also worth noting the 27% growth in advertising revenues, almost doubling the total revenues growth rate. The advertising growth is primarily due to the inclusion of $168 million in revenue related to the Momondo Group for 2018, compared to $72 million in 2017 (it was acquired in July 2017).

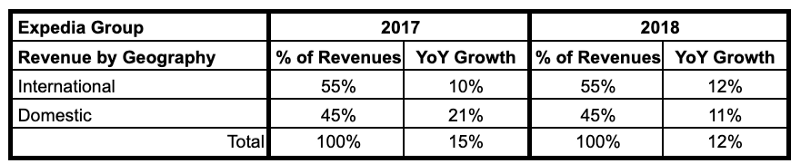

2.2. Expedia Group

Expedia revenues grew 12% in 2018. The group’s core OTA revenues grew slightly less (11%). Homeaway was the business unit with the highest growth (29%), while Trivago had a year on year decrease of 7%.

Expedia’s core OTA revenues in 2018 were 75% of total revenues, same as in the previous year. Homeaway’s share of group revenues continues to climb, reaching 10% in 2018, while Trivago’s declined from 11% in 2017 to 9% in 2018.

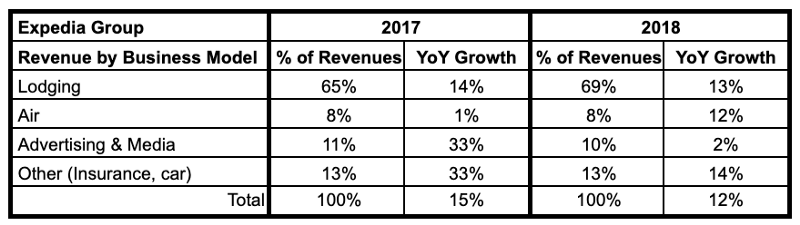

On a revenue by product basis, lodging accounted for 69% in 2018 (up from 65% in 2017), air accounted for 8% (same as in 2017), advertising and media accounted for 10% (down from 11%), and all other revenues accounted for the remaining 13%.

Lodging revenue increased 13% in 2018 on a 13% increase in room nights stayed. Air revenue increased 12% in 2018 on a 5% increase in air tickets sold and a 7% increase in revenue per ticket. Advertising and media revenue increased 2% driven by growth in Expedia Group Media Solutions that offset the decline in Trivago revenues. Other revenue increased 14% in 2018 reflecting growth in the travel insurance and car rental products.

International revenue represented 55% of total revenue in 2018 (same as in 2017), growing 12% year on year, (including 1 percentage point of positive foreign exchange impact). Domestic revenue growth slowed down from 21% in 2017 to 11% in 2018.

2.3. Ctrip

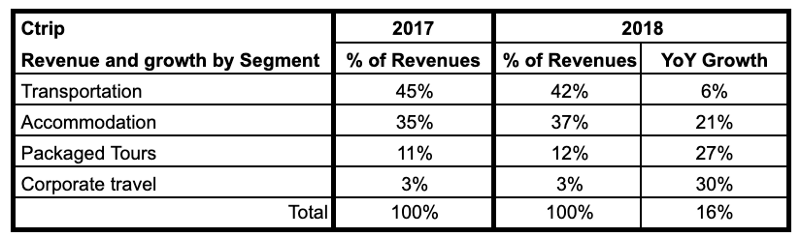

With a 42% share of total revenues in 2018, transportation revenues remains the largest segment, although it has decreased from 45% in 2017. The Accommodations and Packaged Tours segments have gained share vs 2017, and now account for 37% and 12% of total revenue respectively.

Ctrip saw a 16% increase in net revenue in 2018. Transportation, Ctrip’s largest product segment, had the lowest year-on-year growth rate with just 6%. Accommodations, Packaged Tours and Corporate travel saw year on year growth rates of 21%, 27% and 30%.

Ctrip’s international businesses sustained robust growth momentum. In the fourth quarter of 2018, revenue generated from international business made up around 1/3 of group revenue.

2.4. eDreams Odigeo

Includes 4 OTAs brands: eDreams, GoVoyages, Opodo, Travellink. And one metasearch: Liligo.com

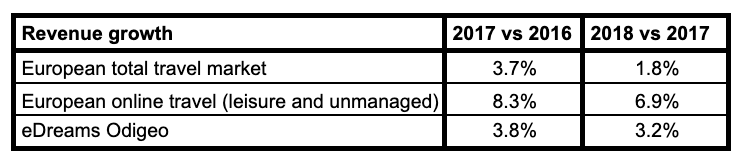

eDreams Odigeo is in the lackluster growth category, with 3.2% revenue growth in 2018. This growth is less than half the rate of European online travel, and barely keeping up with the total European travel market growth rates. This said, it’s much better than European metasearch Trivago (-12%), Indian OTA MakeMyTrip (-18%) and Latam’s Despegar (0.2%). And eDreams Odigeo has proven to be able to consistency grow revenues with high EBITDA margins.

In Q2-Q4 2018 period, EBITDA fell by 11% year on year. In this period, bookings fell by 12% in eDreams Odigeo’s core markets and grew 6% in expansion markets, which points to a significant market share loss in its traditionally strongest markets.

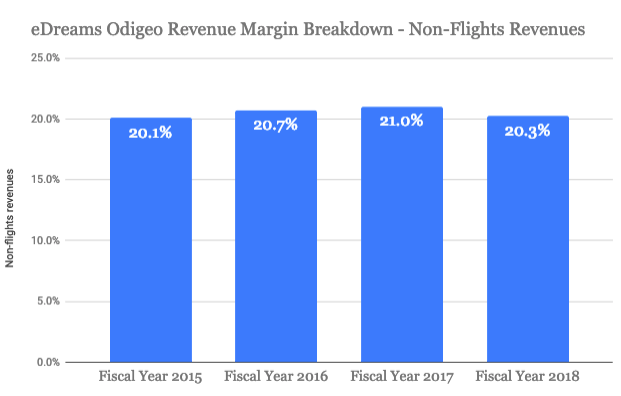

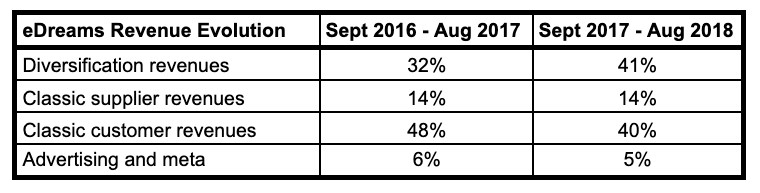

The company has stated that one of its strategic goals for the last 5 years has been to diversify its revenues away from flights, but results don’t show much success on this front.

eDreams Odigeo provides another breakdown of revenues that shows an increase in “diversification revenues”. The company’s definition of “diversified revenues” (flight ancillaries, travel insurance, flight commissions…) still directly depends on the company’s ability to continue to drive flight bookings.

Marketing effectiveness ratio (marketing expenses / revenues) in calendar year 2018 was 64.8% (spends $64.8 in marketing to generate $100 in revenues), the highest among all OTAs in this analysis. It is also 6 percentage points worse than in 2013 and 5 percentage points worse than in 2017. This high marketing expense ratio (compared to the industry) can be explained in large part by eDreams’ flight product specialization. For this same reason, eDreams has also one of the highest EBITDA margins in the industry. The only other OTAs that have a better EBITDA margin than eDreams are Booking and OnTheBeach.

2.5. Despegar.com

After a 27.5% revenue growth in 2017, Despegar’s revenue growth fell sharply to 0.2% in 2018. EBITDA also went from +84% in 2017 to a 24% fall in 2018. These bad results were strongly impacted by currency devaluation (mainly in Argentina) and also by a macroeconomic crisis in Argentina, Despegar’s largest market. Controlling for foreign exchange fluctuations, revenues were up 22% in 2018. Excluding Argentina, adjusted EBITDA was up by $9 million YoY in 2018.

A look at transactions and gross bookings by country and also by currency shows how Argentina and currency devaluation dragged down overall results.

Mobile transactions were up 34% in 2018, accounting to 36% of total transactions (30% in 2017).

Despegar has successfully diversified its revenue mix away from flights. Revenue from hotels and packages represented 50% of total revenues in 2016, 54% in 2017 and 60% in 2018.

2.6. Lastminute Group

Includes 6 OTAs: Lastminute.com, Bravofly, Volagratis, Rumbo, Crocierissime.it, Weg.de. And 2 metasearch: Jetcost and Hotelscan.

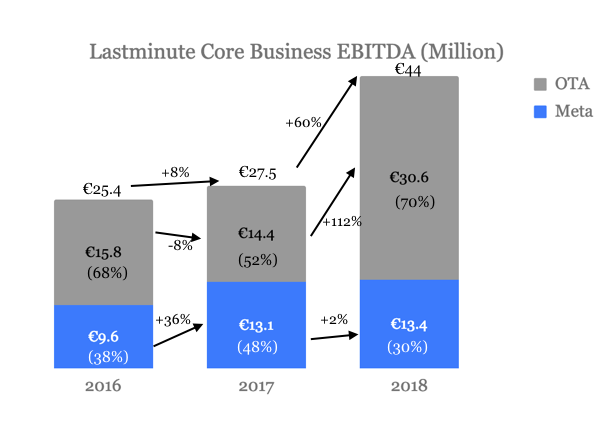

Lastminute had a strong year in 2018, growing revenues by 14.2% and core business EBITDA by 60% while showing clear signs of succeeding in their declared goal of diversifying away from flights.

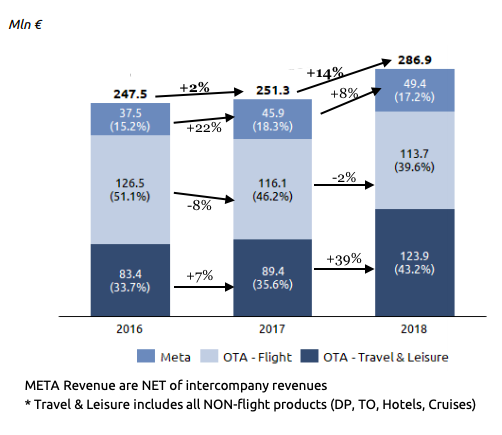

For the first time, Lastminute Group’s 2018 Travel & Leisure revenues (DP, TO, Hotels, Cruises) were higher than their flight revenues, with an impressive year on year growth of 39%. Travel & Leisure revenues now represent 43% of total revenues (up from 35.6% in 2017), vs 39.6% for Flights (down from 46.2% in 2017) and 17.2% for Meta.

As we see in the graph above, OTA Travel & Leisure revenue grew by a very strong 39%, reaching €123.9 million in 2018, €34.5 million more than in 2017. Dynamic packages are a very strong contributor, with almost 50% of Travel & Leisure revenues in 2018.

Lastminute’s core business EBITDA grew by 60% in 2018, driven by a +112% EBITDA growth of its OTA business. What is behind this impressive growth is Weg.de (adding €7.6 million in EBITDA) and OTA organic growth (adding €8.5 million) mostly as a result of Dynamic Package growth.

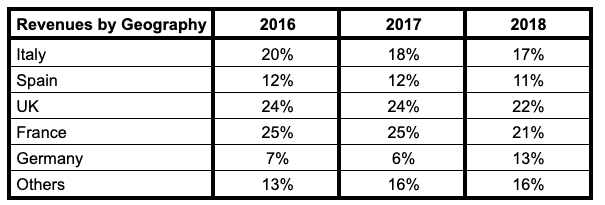

The integration of Weg.de, the german package holidays OTA acquired by Lastminute late in 2017, is evident by the shared captured by Germany of total Lastminute’s revenues.

As we saw in section 1.2, Lastminute is now part of the travel companies with a strong double digit EBITDA/Rev margin.

2.7. MakeMyTrip

From a top and bottom line perspective, calendar year 2018 (FY ends in March) was a disappointing year for the Indian leading OTA: 18% fall in revenues and a negative EBITDA of $172 million (although a 16% improvement vs 2017). This EBITDA is particularly worrisome given that MakeMyTrip decreased its marketing spend by 44% in 2018, after doubling it bot in 2016 and 2017.

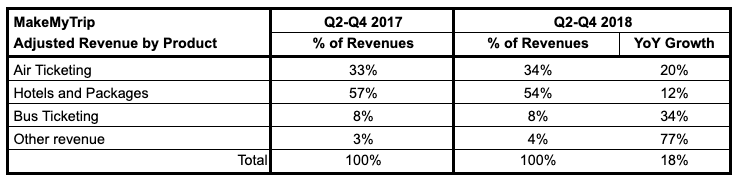

Looking at Q2–Q4 2018, we can see that the revenue decrease was caused by a revenue fall of 48% in MakeMyTrip’s hotels and packages product. Its share of total revenues went from 67% in the 2017 period down to 49% in 2018. The other products had a year on year increase.

MakeMyTrip has not had a positive EBITDA in any of the years included in this report (2013–2018), a troubling situation for a company that has the largest market share in India and that has been operating for 18 years.

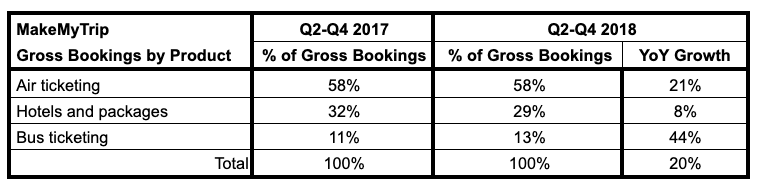

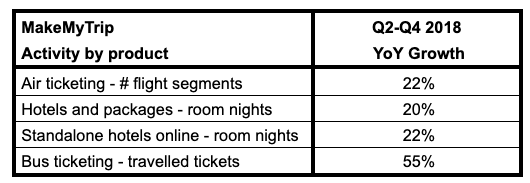

MakeMyTrip also reports “adjusted revenues”, which represents IFRS revenue after adding back promotion expenses (customer discounts, customer acquisition costs, loyalty programs costs). Analyzing the evolution of adjusted revenues, gross bookings, and product activity (air segments, room nights, bus tickets), we do see a growth story.

2.8. On The Beach

On The Beach is a UK online retailer specialized in short haul beach holidays. In 2017, it expanded into Sweden and Norway and in 2018 it acquired Classic Collection Holidays (for £20m)and launched in Denmark. With Classic Collection, On the Beach has now a B2B channel through which they can access millions of short haul beach holidays that had traditionally only been accessible offline.

On the Beach is the smallest in revenues among the 10 companies, but the one with the highest year on year revenue growth (24.5%). It also has a larger EBITDA than Lastminute, MakeMyTrip and Trivago. Part of this growth however, is explained by Classic Collection, the B2B business acquired in 2018.

On the Beach’s branded and free traffic increased to 63.9% of overall traffic, up from 59.3% in 2017. This is a significant share which allows the company to grow organically, while also investing in performance marketing for additional growth. The shift towards a greater share of branded and free traffic is reflected in the company’s continuous improvement in its efficiency ratio (marketing / revenues): 48% in 2016, 44% in 2017, 36% in 2018.

After significant growth of 51% in the first half of 2018, International revenue (Sweden, Denmark, Norway) decreased by 5.9% for the full year. Revenue was heavily impacted by an unusually hot summer in Scandinavia leading to lower demand for holidays and widespread discounting of distressed product by Sweden’s leading tour operators.

2.9. TripAdvisor

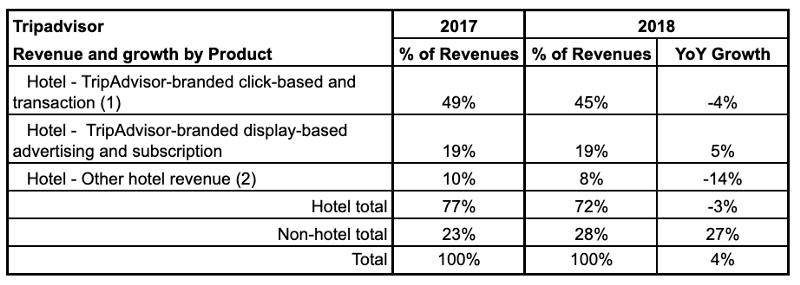

Hotel-based revenue has lost very significant ground since 2016. It has gone from representing 80.4% of total TripAdvisor revenues in 2016, to 77% in 2017 to 72% in 2018. Not only has the share decreased, but also the revenue amount went down by 4%. Looking at the hotel subcategories, it is the click-based hotel revenue that is responsible for this decrease. The display-based hotel advertising actually grew by 5% in 2018. It is evident that both the intended conversion to a metasearch and direct booking model has not produced the desired effects.

TripAdvisor’s non-hotel revenues, on the other hand, saw a solid 27% year-on-year growth in 2018. They are now responsible for 28% of total revenues, 5 percentage points more than in 2017. Three product lines are included in the non-hotel revenues: experiences, restaurants and alternative accommodations. Experiences and restaurants grew by 40% in 2018, while alternative accommodations dragged down the growth of the non-hotel segment to 27%. Alternative accommodations apparently is no longer a strategic focus for the company given the very strong competition that they face from the likes of Airbnb and Booking.com. Skift reported that TripAdvisor is considering a new way of reporting its earnings in order to “be able to isolate the robust growth of experiences and restaurants”.

TripAdvisor continues to invest in its experiences business. On April 2018, one day after Booking announced the acquisition of FareHarbor (a tours and activities tech provider), TripAdvisor announced the purchase of Bokun, an Iceland-based technology provider for tours, attractions and experiences. As a result, TripAdvisor had a 60% increase in experience providers and 90% increase in bookable products in 2018.

2.10. Trivago

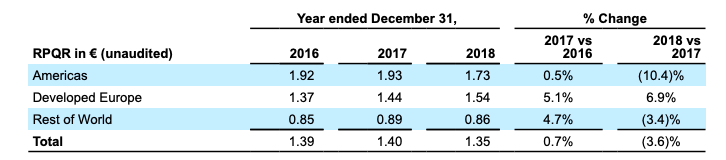

Trivago revenue decreased by 11.6% in 2018 as a result of an 8% drop in Qualified Referrals (1 QR = Trivago visitor click on an OTA or supplier direct product offer) and a 3.6% lower Revenue per Qualified Referral (metric that measures how effective Trivago is in monetizing the leads sent to advertisers). Europe had the biggest decrease in referrals sent to advertisers, but its RPQR grew due to a favorable exchange rate fluctuation.

On the marketing front, Trivago reduced its advertising spend by €152 million or 17.2% in 2018 compared to 2017. It focused on reducing brand marketing expenditures and increasing the return of performance marketing campaigns. Of all the companies in this analysis, Trivago has the highest ratio of marketing costs / revenues, at 80% (down from 85% in 2017).

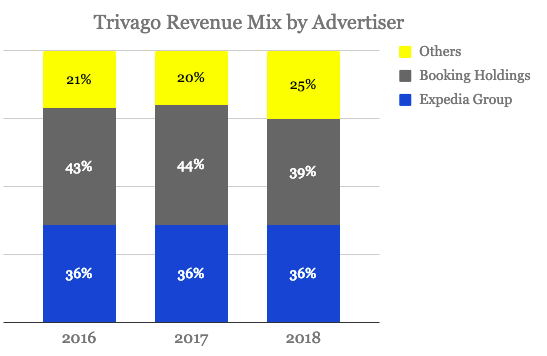

Trivago continues to generate the majority of its revenues from the largest two OTA: Booking Holdings (Booking.com, Agoda, etc…) and Expedia Group (which owns Trivago).

Despite falling revenues, Trivago increased its adjusted EBITDA from €6.7 million in 2017 to €15.6 million in 2018. Trivago expects a continued improvement in EBITDA in 2019, estimating to close the year between €50 million and €75 million.

Trivago remains at a different category vs. its metasearch peer TripAdvisor in its limited ability to generate EBITDA and revenue growth. This is worrisome for a company which has been around for 14 years.

Notes

–Expedia: Data for Marketing Costs field is Direct Selling and Marketing (adjusted selling and marketing). Not including Indirect Selling and Marketing. Adjusted EBITDA

–Booking: Data for Marketing Costs field is Performance Advertising + Brand Advertising. Not including Indirect Sales and Marketing Costs. Data for EBITDA field is Adjusted EBITDA.

–eDreams: Fiscal year ends March of the following year. eDreams data shown for 2017 and 2018 is calendar year (adding the 4 calendar year quarters). Data for Revenues = Revenue Margin. Data for Marketing Costs = Variable Costs. Adjusted EBITDA.

–Lastminute: Revenue reported in 2014 and 2015 is Group Revenue. In 2016, 2017 and 2018 it is Core Business Revenue. For 2014–2015 Adjusted EBITDA figures. For 2016–2018 Business EBITDA figures.

–Tripadvisor: Data for Marketing Costs = Selling & Marketing Direct Costs (includes stock based compensation expenses). Data for Ebitda is Total Adjusted Ebitda

–Trivago: Data for Marketing Costs = Advertising expense for annual data. Revenue is total revenue: related parties + third parties.

–MakeMyTrip: Fiscal year ends march of the following year. Annual 2017 and 2018 is calendar year (adding the 4 quarters).

–Ctrip. Marketing = Sales and marketing

–Despegar. Selling and marketing

–On The Beach: Fiscal year ends September.